To be truly actionable, a good housing study relies on a detailed and nuanced quantitative model of housing market trends. There are many ways to approach this task, but the most effective method focuses on modeling housing preferences to predict the choices local households would make if given the options most suited to their needs.

Conventional approaches to modeling housing markets

Planners employ a variety of methods to understand housing needs and predict market dynamics. All have merit but most have blind spots that can make their results misleading. Two of the most common include:

- Local patterns and comparables: Analyzing recent patterns in the local housing market can help identify trends that might extend into the future. However, this approach can be misleading without connection to the broader context because local observations are constrained by the units and households that arbitrarily happen to exist within that locality. Households that move out or otherwise prefer a locally underrepresented housing type or price point but are settling for what is available might be mischaracterized or pass under the radar altogether. It would be better to understand their perspective within a context that considers all the housing options available to them, regardless of jurisdictional boundaries.

- Migration and buying power: Especially when considering emerging housing market demand, understanding the nature of new households entering – or potentially entering – the local market can help identify the unit types and price points most likely to attract and retain them locally. However, when estimating prices, a critical step in the process of calibrating new targeted development, this approach often assumes all households are willing to pay the same percentage of their income on housing, potentially overstating demand at some price points and understating at others. In reality, different households at the same income level might be willing to pay significantly different amounts on housing, stretching their budgets in some cases and acting frugally in others. It would be better to assign a probabilistic distribution of price points to each income level that better reflects real-world variation in willingness to pay.

An approach to empirically measuring housing preferences

CommunityScale has developed a new method to more accurately quantify housing preferences that learns from and improves upon the conventional approaches described above. At its core, the method empirically measures recent housing purchasing behavior to quantify the range of housing types and price points households of different income levels are likely to choose in a given locality.

The following key approaches make this a better approach for understanding housing preferences and predicting housing market behavior.

- Regional context: We measure and catalog the recent purchasing decisions of households across the broader region, providing a geographically unconstrained market context that can characterize the choices households make regardless of what is or isn’t available in a given municipality.

- Willingness to pay: We measure how much households at all income levels who have recently moved are choosing to pay for housing relative to their total income. Rather than averaging this into a single factor for each income level, we catalog the full distribution of costs for each income level and apply this to our needs assessments to retain sensitivity to the fact that different households with the same income do not pay the same amount for housing.

Applied to our housing study work, this approach allows us to estimate what housing types current and future households need and how much they are willing to pay with more nuance and sensitivity than more conventional methodologies.

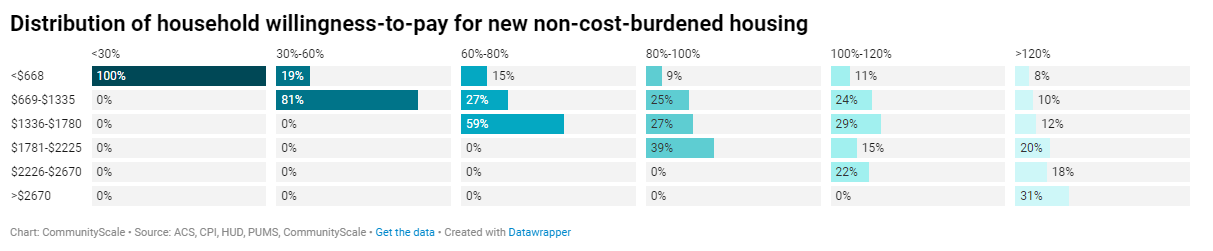

The table above illustrates the distribution of housing costs households at different income levels are likely to choose (with a control in place to avoid assigning units to households that would create new cost burden). With the exception of households earning <30% AMI, all income levels include households willing to pay a variety of monthly costs for housing. At lower incomes, these costs trend closer to the 30% cost burden threshold. At higher incomes, a minority of households are willing to pay more than 20% or 25% of their income on housing. Overall, there is much more diversity in willingness to pay than a conventional modeling approach would recognize.

CommunityScale’s approach to measuring housing preferences gives our housing study work much more sensitivity to the nuances behind the housing decisions local and regional households make, providing more predictive power and accuracy for our clients.